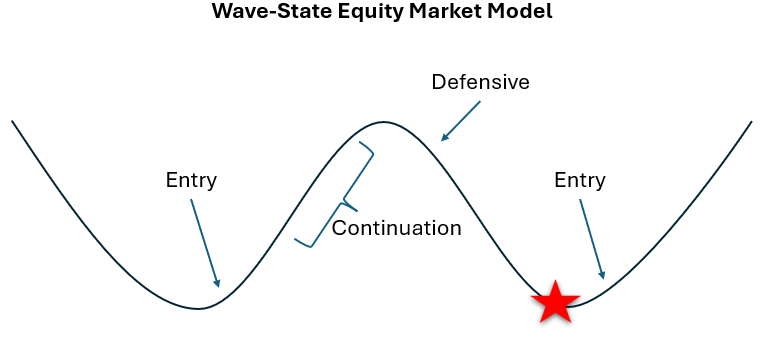

Defensive Shift Protects Downside

The ROQ Wave-State Model shifted to a Defensive posture at the open of May 12, completing a textbook transition that began with the first deteriorating signal on May 8. What made this transition notable wasn't just the outcome, it was the process.

The two-day cooldown rule is designed precisely for moments like this. When the signal first turned negative on May 8, the model held its Bullish Continuation allocation rather than reacting immediately. May 11 confirmed the deterioration, satisfying the cooldown and triggering the transition at the following open. That discipline was validated almost immediately: May 14 produced a brief one-day bounce in both indicators that looked like a potential recovery. Without the cooldown rule, the model would have rotated back to a growth posture, only to reverse sharply the very next day when the defensive signal resumed. The rule earned its keep.

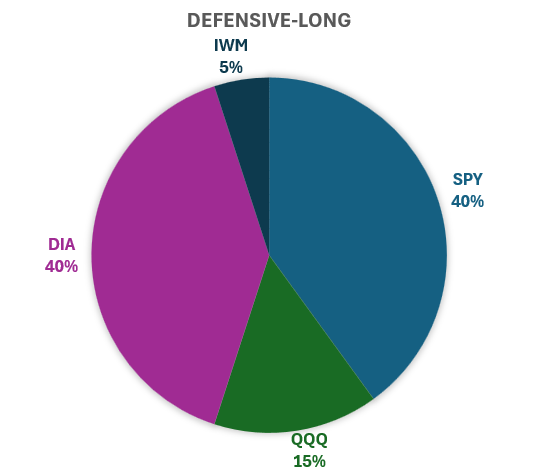

The Defensive allocation (40% SPY, 40% DIA, 15% QQQ, 5% IWM) isn't a retreat from the market. The portfolio remained fully invested throughout, rotating toward a more balanced, stability-oriented mix. That positioning cushioned the week's roughest day on May 15, when a broad selloff hit small caps particularly hard, without sacrificing participation on the positive days earlier in the week.

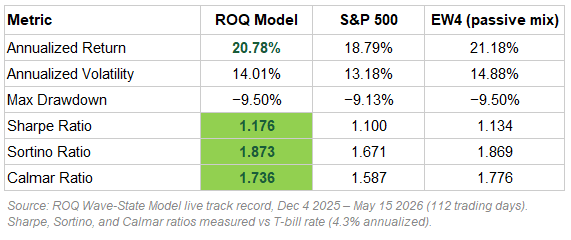

Now 112 trading days into the live track record, the numbers are beginning to tell a story worth examining:

The comparison to SPY is straightforward: better return, better risk-adjusted performance across every measure. The comparison to EW4 requires a bit more context. EW4 is a passive, equal-weighted mix of the same four ETFs the model uses, rebalanced daily and never adjusted. It’s slightly higher raw return reflects a permanent tilt toward the more aggressive names in the portfolio. The model, by design, periodically rotates away from those names when conditions deteriorate.

What the numbers show is that this tactical rotation, the active work the model does, produces a comparable risk-adjusted result to simply holding everything equally, while doing so with meaningfully less day-to-day volatility. The model's Sortino Ratio of 1.873 essentially matches EW4's 1.869 with 87 basis points less annualized volatility. That is the early signature of the tactical approach working: similar reward, smoother ride.

The more compelling test will come in a genuine sustained downturn. EW4's permanent overweight to the high-octane names will amplify losses in that environment in a way the model's Defensive rotation is specifically designed to avoid. That chapter hasn't been written in the live period yet — but the mechanics are in place and, as this week demonstrated, functioning as intended.

The signals will tell us when conditions improve enough to shift back to offense.

Market analysis and this blog post were conducted and written with the assistance of AI analysis under human oversight.

The information provided here is for educational and informational purposes only and should not be considered financial advice. I am not a licensed financial advisor, and my portfolio may not be appropriate for your financial goals or risk tolerance. All investments involve risk, including the potential loss of principal. Historical data and market models are not indicative of future results. Please consult with a licensed financial professional before making any investment decisions.