A New Version, A New Signal

The ROQ Wave-State Model has done exactly what it was designed to do since its inception in December 2025. By rotating tactically between a defensive allocation and a growth-oriented allocation, guided entirely by the internal structure of the market rather than price prediction, the portfolio has outperformed the S&P 500 through allocation discipline alone. Just systematic rotation based on measurable probabilities derived from the signal.

That foundation is solid. And after several months of live operation, I went back to the data to ask whether the model could be improved.

The Upgrade

After extensive backtesting across ten years of historical data, I've revised the ruleset that governs ROQ portfolio construction. Version 3.0 expands the conditions under which the model will deploy leverage, adds a hard volatility gate requiring VIX below 20 at any leverage entry, and introduces a signal-based exit stop that automatically removes leverage if both indicators deteriorate simultaneously for two consecutive days. The result is a more responsive model with better downside protection built in.

The numbers speak for themselves. Against the S&P 500 over ten years:

Cumulative return: V3.0 +692% vs S&P 500 +239%

Annualized return: V3.0 23.2% vs S&P 500 13.1%

Maximum drawdown: V3.0 −34.7% vs S&P 500 −34.1%

Sharpe Ratio: V3.0 0.916 vs S&P 500 0.485

Sortino Ratio: V3.0 1.176 vs S&P 500 0.588

Calmar Ratio: V3.0 0.544 vs S&P 500 0.258

Better returns. Better risk metrics. Same maximum drawdown (which occurred during the COVID-19 pandemic.) Every metric improved without adding tail risk. That's a rare combination and the reason I'm confident making the change.

I applied V3.0 retroactively to the actual live period data that the model had never seen. It would have returned +15.82% versus the +11.42% actually recorded, with the additional return coming from four specific leveraged days the original criteria missed. That out-of-sample check gave me the confidence to move forward.

Today's Signal

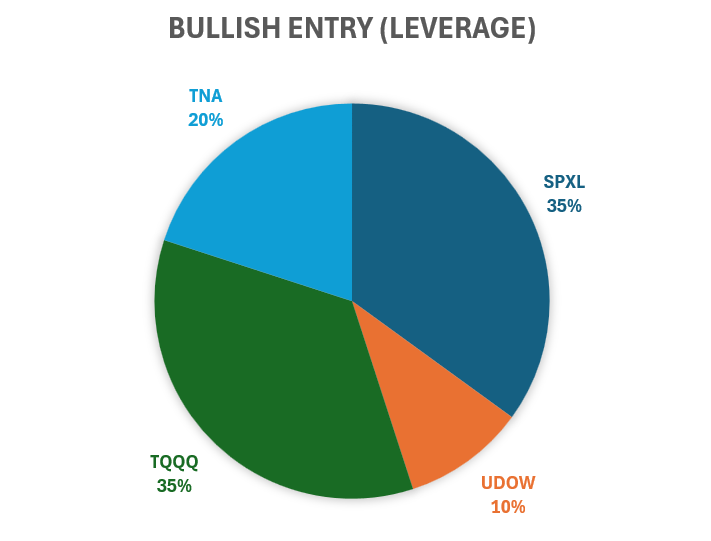

This week, the model produced its first Bullish Entry signal under V3.0 criteria. After nearly three weeks of base-building, the momentum indicator was grinding along deeply oversold levels while the market moved modestly higher. Both the breadth signal and momentum turned up sharply on Wednesday, confirmed on Thursday, and the leveraged position was engaged at Friday's open. VIX was sitting at 16.90, well clear of the gate. The setup was clean.

Friday returned +1.19% on the leveraged portfolio versus the S&P 500's +0.39%. The position remains open heading into next week, with both indicators still rising and the stop not triggered.

Where Things Stand

ROQ Portfolio (inception to date): +11.29%

S&P 500: +8.90%

EW4 Passive Benchmark: +10.81%

Market analysis and this blog post were conducted and written with the assistance of AI analysis under human oversight.

The information provided here is for educational and informational purposes only and should not be considered financial advice. I am not a licensed financial advisor, and my portfolio may not be appropriate for your financial goals or risk tolerance. All investments involve risk, including the potential loss of principal. Historical data and market models are not indicative of future results. Please consult with a licensed financial professional before making any investment decisions.