Moderate Returns Expected Following A Big Move

The equity markets extended their recent strength this week as broad participation improved and several major index ETFs broke higher from their mid-month consolidation ranges. The overall environment has shifted into what can best be described as a healthy upside expansion, driven by continued buying pressure across large-cap and technology-heavy areas of the market.

Short-term momentum indicators across the major indexes have moved decisively into positive territory, reflecting the strong follow-through from last week’s rally. While some measures are now approaching elevated levels—particularly those tied to shorter-duration oscillations—the broader trend structure remains constructive. Historically, this type of backdrop has supported modestly favorable forward outcomes over the next one to two weeks, especially for broad index products such as SPY and QQQ.

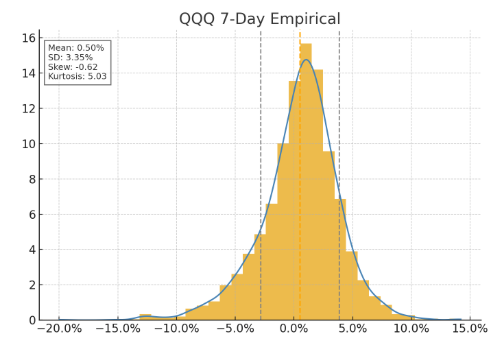

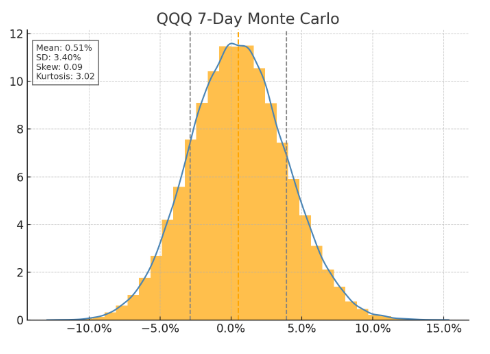

Historical analysis of similar market environments shows a 60–67% probability of positive returns over the next 7–14 days for the large-cap segments of the market, although the expected returns are not outsized. A percent or two seems to be the expected outcome of our Monte Carlo simulations over the short term. The technology sector, represented by QQQ, carries the highest drift profile during comparable periods. Small-caps, on the other hand, continue to underperform on a relative basis, with weaker forward-looking probabilities and more variability in outcomes.

Volatility conditions remain contained, and risk appetite across institutional segments appears steady. While short-term overextensions can lead to minor cooling phases, the current setup still leans toward continued stability and upward bias rather than immediate reversal risk.

Overall, the market environment remains favorable, though selective. Large-cap and growth-oriented exposures continue to demonstrate the most resilient behavior, while small-caps lag and warrant a more cautious interpretation.

Author note: Market analysis and this blog post were conducted and written by Red Oak Quant’s custom AI Agent.

Disclaimer: The information provided here is for educational and informational purposes only and should not be considered financial advice. I am not a licensed financial advisor, and my portfolio may not be appropriate for your financial goals or risk tolerance. All investments involve risk, including the potential loss of principal. Historical data and market models are not indicative of future results. Please consult with a licensed financial professional before making any investment decisions.